Travel

Big Bus Tours San Francisco Reviews: A Comprehensive Look

The feeling of finally paying off your mortgage is exhilarating. It’s a significant accomplishment, but it also begs the question: paid off house now what? With 60% of homeowners facing the same dilemma, it’s important to understand that the journey doesn’t end there. This article will guide you through the next steps, from managing ongoing homeownership expenses to exploring new financial opportunities.

Congratulations on reaching this remarkable milestone! Paying off your mortgage is no small feat; it signifies years of dedication, hard work, and financial discipline. The emotional and financial benefits of being mortgage-free are profound. You can now enjoy the peace of mind that comes with knowing you own your home outright, free from monthly mortgage payments.

This newfound financial freedom opens up a world of possibilities. With your mortgage eliminated, you have the flexibility to allocate your funds elsewhere—whether that’s investing in your future, saving for retirement, or pursuing personal goals. Take a moment to celebrate this achievement. Consider hosting a small gathering with family and friends to share your success and reflect on the journey that brought you here. Celebrating this milestone can reinforce your motivation to continue making sound financial decisions moving forward.

While your mortgage payment is gone, it’s essential to remember that homeownership comes with ongoing expenses that require careful management. Understanding these costs will help you navigate the post-mortgage landscape effectively.

Even without a mortgage, property taxes remain a significant expense. Depending on your home’s value and location, these taxes can vary widely. It’s wise to set aside funds regularly to cover this bill when it comes due. Consider creating a dedicated savings account for property taxes to avoid any surprises.

Property taxes can fluctuate due to changes in local tax rates or property assessments. Staying informed about your local tax laws can help you anticipate any changes in your tax obligations. Additionally, consider appealing your property tax assessment if you believe it is higher than it should be. This can potentially save you a significant amount of money in the long run.

With your home fully owned, maintaining adequate homeowners insurance is essential. This coverage protects your investment and provides peace of mind against unforeseen events. Review your policy to ensure it meets your current needs and consider any changes that may arise after paying off your mortgage.

Your insurance needs may change as your home appreciates in value or as you make improvements. Regularly reassessing your coverage can help ensure that you are not underinsured. You might also explore options for bundling your insurance policies to save on premiums.

Owning a home means dealing with maintenance and repairs. From routine upkeep to unexpected emergencies, these costs can add up quickly. Allocate a portion of your budget for regular maintenance tasks, such as lawn care, HVAC servicing, and general repairs. It’s also a good idea to set aside funds for larger projects, like roof replacements or renovations, which can be costly.

Establishing a home maintenance schedule can help you stay on top of these tasks. Regularly inspecting your home for wear and tear can prevent small issues from becoming major problems. Additionally, consider creating a maintenance fund specifically for unexpected repairs to avoid financial strain when emergencies arise.

If your property is part of a homeowners association, be prepared for ongoing fees. These dues cover shared amenities and community maintenance. Ensure you factor these costs into your budget to maintain financial stability. Understanding the services provided by the HOA can help you determine if the fees are justified.

If you find that the HOA fees are increasing or that you are not receiving adequate services, consider discussing your concerns with the association. Engaging with your community can lead to improvements in the services provided and may even influence future fee structures.

By planning ahead for these ongoing expenses, you can avoid financial strain and ensure your home remains a source of comfort and security.

With your mortgage gone, you may find yourself with a significant increase in disposable income. This newfound financial freedom opens doors to various opportunities for utilizing your extra money effectively. Here are some options to consider:

If you have other debts, such as credit cards or student loans, consider using your additional income to pay them off. Reducing your overall debt load can improve your financial health and free up even more funds for future investments. Paying off high-interest debts first can provide the most significant financial relief.

A debt reduction strategy can include methods such as the snowball or avalanche approaches. The snowball method focuses on paying off the smallest debts first for quick wins, while the avalanche method prioritizes debts with the highest interest rates. Choose a method that aligns with your financial goals and psychological comfort.

An emergency fund is a financial safety net that can protect you against unforeseen expenses. Experts recommend having three to six months’ worth of living expenses saved. With your mortgage payment eliminated, you can prioritize building or supplementing this fund, providing peace of mind for unexpected situations.

Consider setting up a high-yield savings account specifically for your emergency fund. This allows your savings to grow while remaining easily accessible in case of emergencies. Automating transfers to this account can help you consistently contribute to your fund without having to think about it.

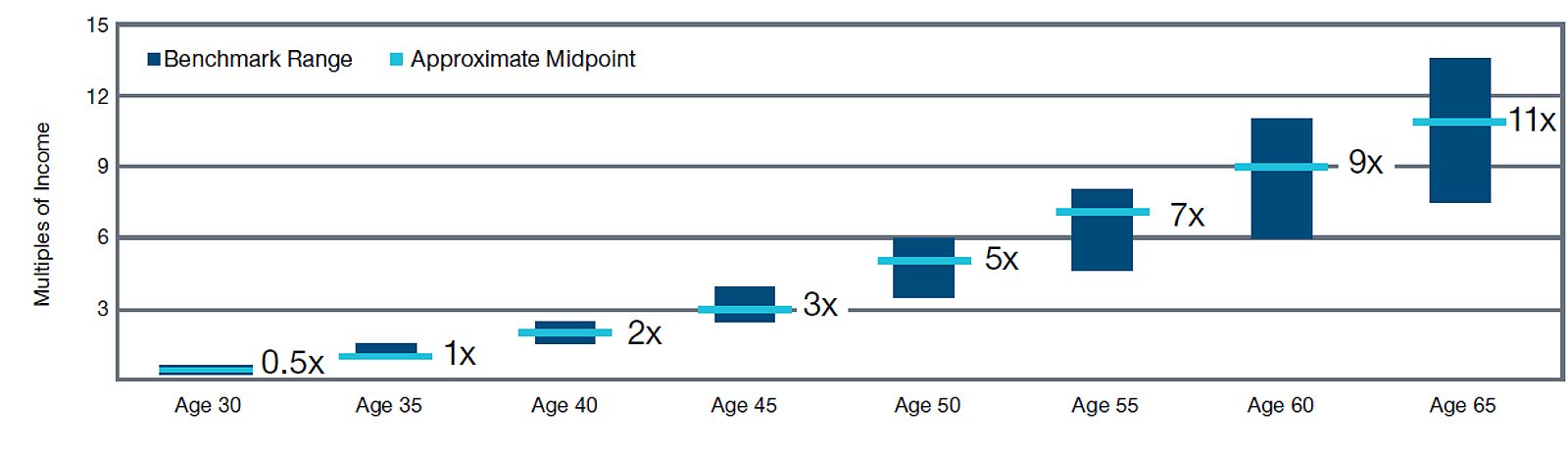

Now is the perfect time to focus on your retirement savings. If you haven’t already maxed out your contributions to retirement accounts, consider doing so. This is especially important for individuals aged 50 and over, who have access to “catch-up” provisions that allow for higher contributions.

Review your retirement plans to ensure you are taking full advantage of employer matching contributions. If your employer offers a 401(k) plan, consider increasing your contributions to maximize the benefits. Additionally, explore other retirement accounts, such as IRAs, to further enhance your savings.

Investing can be a great way to grow your wealth over time. With your mortgage paid off, you may feel more comfortable allocating funds to a diversified investment portfolio, including stocks, bonds, or real estate. Research various investment options to find those that align with your risk tolerance and financial goals.

Consider consulting with a financial advisor to develop an investment strategy that suits your needs. They can help you navigate the complexities of the market and provide guidance on asset allocation, risk management, and diversification.

The extra money from your mortgage payment can also be used to pursue personal goals. Whether it’s traveling, furthering your education, or exploring new hobbies, this is an opportunity to invest in experiences that enrich your life. Setting aside funds for personal development can lead to a more fulfilling life.

Reflect on what matters most to you and how you can allocate your resources to support those goals. Whether it’s taking a course, starting a new business, or simply enjoying a well-deserved vacation, investing in yourself can yield significant returns in happiness and satisfaction.

By thoughtfully considering how to utilize your extra money, you can enhance your financial future and achieve your personal aspirations.

To make the most of your post-mortgage life, consider implementing strategies that can help you maximize your financial potential. Here are some suggestions:

With your mortgage paid off, it’s essential to review your insurance coverage. Ensure that you have adequate life, disability, and long-term care insurance. This can provide additional security for you and your loved ones, especially if unexpected circumstances arise.

Evaluate your insurance needs periodically to ensure they align with your current life situation. Major life events, such as marriage, having children, or changes in employment, may necessitate adjustments to your coverage.

Investigate different investment opportunities that can provide favorable returns. Whether it’s real estate, stocks, or mutual funds, diversifying your investments can help you build wealth over time. Take the time to research and understand each option to make informed decisions.

Consider attending workshops or seminars on investing to enhance your knowledge. Engaging with other investors can also provide valuable insights and ideas for potential investments.

Consider seeking professional advice from a financial advisor. They can help you develop a personalized financial plan tailored to your specific goals and circumstances. A financial advisor can provide insights into investment strategies, retirement planning, and overall financial management.

Working with a financial advisor can help you navigate complex financial situations and provide accountability as you work toward your goals. This partnership can be invaluable in achieving long-term financial success.

Real-life examples abound of individuals who have successfully navigated their post-mortgage lives by implementing these strategies. By being proactive and informed, you can position yourself for financial success.

What should I do first after paying off my mortgage?

Start by assessing your ongoing expenses, such as property taxes and insurance, and create a budget that accounts for these costs. Then, consider how to allocate any extra funds toward debt reduction, savings, or investments.

How can I ensure I don’t overspend now that my mortgage is paid off?

Establish a detailed budget that outlines all your expenses, including ongoing homeownership costs. This will help you manage your finances and prevent overspending.

Is it wise to invest all my extra money after paying off my mortgage?

While investing is important, it’s also essential to build an emergency fund and consider paying off other debts. A balanced approach will help you achieve financial security.

Paying off your mortgage is a remarkable achievement that brings both emotional and financial benefits. As you navigate your post-mortgage life, understanding ongoing expenses and exploring new financial opportunities is crucial. By carefully managing your finances and making informed decisions, you can create a secure and fulfilling future. Remember, the journey doesn’t end here; it’s just the beginning of a new chapter in your financial life. Embrace this opportunity to build a life that aligns with your values and aspirations, and enjoy the peace of mind that comes with being mortgage-free.

MORE FROM pulsefusion.org