Travel

Big Bus Tours San Francisco Reviews: A Comprehensive Look

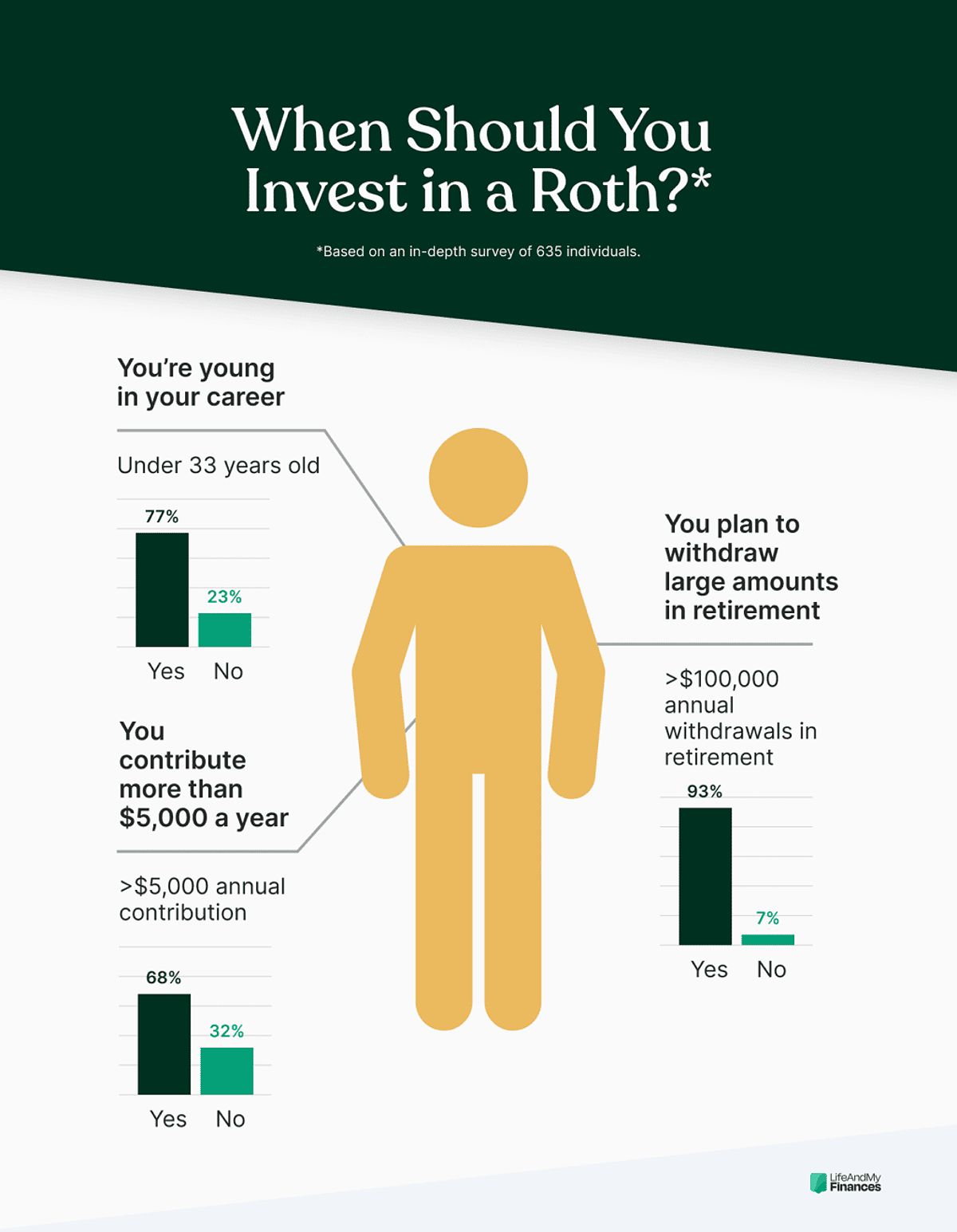

Retirement planning often involves considering a Roth IRA, but a growing number of financial experts are questioning its universal suitability, especially for those nearing retirement. While the allure of tax-free withdrawals during retirement is undeniable, a significant portion of near-retirees find themselves in a position where a Roth IRA might actually be detrimental to their long-term financial well-being. This article delves into the reasons why a Roth IRA may not be the best choice for everyone, particularly those approaching their golden years.

A Roth IRA is often viewed as a golden ticket for retirement savings, primarily due to its promise of tax-free withdrawals when the time comes. However, this perception can be misleading, especially for individuals nearing retirement.

The Roth IRA’s appeal is rooted in its potential for tax-free growth. Contributions are made with after-tax dollars, allowing your investments to grow without the burden of future taxes on withdrawals. For many, this seems like a prudent strategy, ensuring a secure financial future.

The Pros:

The Cons:

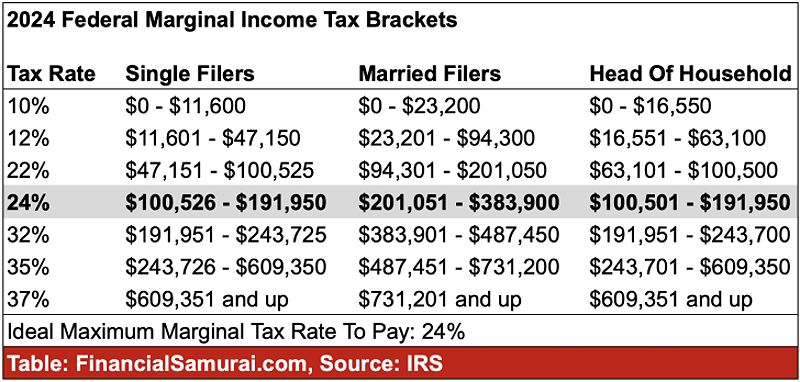

For individuals nearing retirement, the financial landscape often shifts dramatically. Many expect to earn less in retirement, which raises questions about the wisdom of paying taxes now through a Roth IRA.

Key Points to Consider:

A Compelling Example: Imagine a 60-year-old named Sarah who decides to convert her Traditional IRA to a Roth IRA. While she dreams of tax-free growth, the immediate tax liability from the conversion can place a significant financial strain on her. If Sarah finds herself in a higher tax bracket now than she would in retirement, she may end up paying more in taxes than if she had left her money in a Traditional IRA.

While the Roth IRA captures much attention, the Traditional IRA remains a powerful and often overlooked tool for retirement savings. Its tax-deferred benefits can be particularly advantageous for those nearing retirement.

A Traditional IRA allows individuals to contribute pre-tax dollars, effectively reducing their taxable income in the year contributions are made. This immediate tax benefit can be a game-changer for those in their peak earning years.

The Pros:

The Cons:

For many nearing retirement, the Traditional IRA presents several compelling advantages.

Key Points:

A Compelling Example: Consider a 55-year-old named Tom who opts to contribute to a Traditional IRA. By doing so, he not only benefits from immediate tax relief but also positions himself for potentially higher after-tax returns in retirement, especially if his income decreases significantly.

When weighing the benefits of a Roth IRA against a Traditional IRA, several key factors should guide your decision, especially for those approaching retirement.

While Roth and Traditional IRAs are popular choices, there are alternative strategies worth considering for retirement savings.

Annuities can provide guaranteed income streams during retirement, alleviating the pressure to make large withdrawals from IRAs. This can be particularly beneficial for near-retirees who want to ensure a consistent cash flow without the risk of market fluctuations.

For near-retirees, the decision to convert a Traditional IRA to a Roth IRA requires careful consideration. While this strategy can lead to tax-free growth, the timing of the conversion is crucial. Conducting a conversion during a year of lower income can help minimize the tax burden.

Other tax-advantaged retirement accounts, such as 401(k)s and 403(b)s, should not be overlooked. These accounts often come with employer matching contributions, significantly boosting retirement savings.

Navigating the complexities of retirement planning can be challenging, making it essential to consult with a qualified financial advisor or tax professional. Personalized guidance can help you understand the implications of your choices, ensuring that your retirement savings strategy aligns with your individual circumstances and goals.

Given the intricacies involved in choosing between a Roth IRA and a Traditional IRA, professional advice can be invaluable. A financial advisor can help you evaluate your current situation, project future income needs, and recommend the most suitable retirement savings options.

Q: If I’m already contributing to a Roth IRA, should I switch to a Traditional IRA?

A: It depends on your individual circumstances and financial goals. Consider your current tax bracket, projected future tax bracket, and time horizon for retirement. Consulting with a financial advisor or tax professional can help you make an informed decision.

Q: What are the tax implications of withdrawing money from a Roth IRA before age 59.5?

A: You can withdraw your contributions to a Roth IRA tax-free and penalty-free at any time. However, withdrawing earnings before age 59.5 is subject to a 10% penalty and taxes.

In summary, while a Roth IRA may seem like an attractive option for retirement savings, it is essential to weigh the potential drawbacks, especially for those nearing retirement. Factors such as current and future tax brackets, time horizon, and individual circumstances can significantly influence whether a Roth IRA is the right choice. By considering alternative strategies and seeking professional advice, individuals can make informed decisions that align with their financial goals and retirement plans.

MORE FROM pulsefusion.org